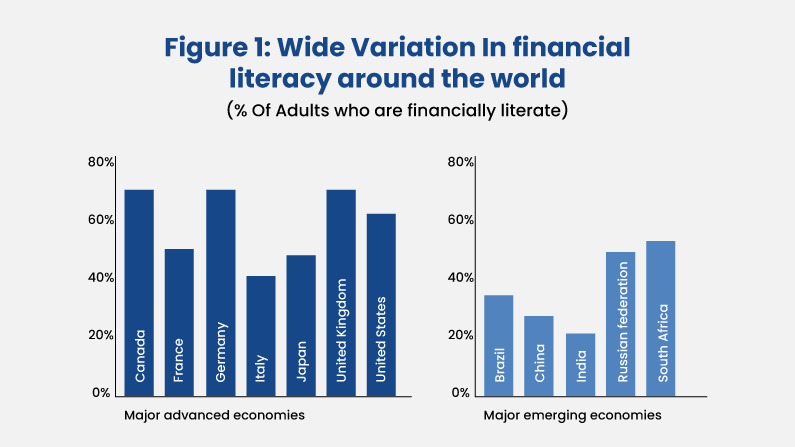

There’s no doubt Canada is one of the world’s leading nations with the most financially literate adults. These stats show more than 65% of Canadians are financially literate. In addition, 56% of young adults (18 years to 35 years) have started to increase their financial literacy. So, if you are one of them, pat yourself on the back!

As more and more Canadians understand the importance of financial literacy, they need to learn from a good source. At PrestoCash, we have been in the finance business for several years. Through our experience and observation, we came across 6 important points that people tend to miss when learning about finances.

Well, it’s also quite natural. For example, what would a person search when he needs a loan on the same day and have a poor credit score? Most likely “How to get same day e-transfer loan in Canada.” Because, in difficult times, people often lose sight of the future and try to fix the present as fast as they can. And it’s not wrong, but to be financially literate, you have to train your mind to stay strong in difficult times.

As Robert Kiyosaki said, ‘If you are not disciplined with your finances, you are at the mercy of your circumstances and creditors.’

The Internet is filled with information, and finding relevant content to help finances can be tricky as no content is shown in proper order. So if you have stumbled on this post, make use of this as best as you can. In your journey to become financially literate, here are 6 important elements you must understand to manage your finances better.

6 Financial Literacy Elements

Budgeting

- The basic principle of budgeting means to allot budget to different aspects of your life. For example, set a budget for your needs, wants, investment, charity, or emergency. How you want to set the budget is entirely on your income and how well you manage your money.

- But, it is a good place to start. Many people who start budgeting have seen a positive change in their finances. These habits make a lifestyle shift and allow you to manage your money better.

Taxes

- Do you also scratch your head when it comes to taxes? Like, how in the world does it work! There is income tax, TDS, then filling a tax return, and how many taxes to pay? What are tax rebates? These all can be frustrating. We know it seems a lot, but after reading this, it won’t!

- Taxes are normal, and everyone has to pay them someday. However, just because your income doesn’t come under any tax slab, you should not keep it for the future. Taxes are important, and unless you are from a commerce background, wrapping your head around it can be difficult but not impossible.

- There are two main types of taxes direct and indirect. Direct: which you pay directly to government and indirect: which you pay via goods and services, for example, dine in a fancy restaurant and check the bill, the final amount has tax added on the total bill, that’s indirect tax.

- The most important for you right now is the income tax. Below are Canada’s federal tax rates as of 2022.

Income (Annual) Tax rate

- Below $50,197 15%

- $50,197 – $100,392 5%

- $100,392 – $155,625 26%

- $155,625 – $221,708 38%

- More than $221,708 33%

- These are the tax slabs for the citizens of Canada. You have to pay taxes based on the slab your income falls under. The taxes are paid at the end of the financial year. You can calculate your taxes using any tax-calculator website and pay them online or in the taxation department. The following image is of a standard tax calculator.

- If you are a job person, you get charged with TDS (Tax Deducted at Source). This is because the company you are working for deducts your tax from your income and pays to the government on your behalf. At the end of the year, you can show your income slip to tax officers as a proof of tax payments.

- If you are a business owner or self-employed, you have to pay taxes on your own. However, you can calculate taxes on a tax-calculating website and pay between the allotted dates. To know more, you can consult a chartered accountant.

Credit

- Credit is a major part of our financial literacy. It’s the same as what makes or breaks you. Every person takes credit at least once in their life, and if you don’t know how to use it wisely, you are one step away from getting into a debt trap.

- Credit has many forms, such as loans, credit cards, postpaid payments or bills, and more. In addition, as you grow older, you will need a vehicle, home, may be planning for a trip or have to fund your or your children’s education, and the most common of all is emergencies, add a bad credit score on top of it.

- Getting a loan with a poor credit score can be difficult. Moreover, a bad credit score reduces your chances of getting a loan in the future. Although, financial institutions such as PrestoCash offer Fast e-transfer loans in Canadawithout a credit check to help you deal with emergencies.

- Indeed, we do not check your credit score. However, we also do appreciate financially literate clients. That’s why we write content along with providing loans to improve your financial knowledge and contribute to the nationwide effort to improve financial literacy among citizens.

- A poor credit score is the reflection of poor knowledge of loans. Although there are many things to learn about loans and managing credit, below are short points that you must consider.

- Do not use more than 30% of your total credit limit.

- Do not gamble with your loan.

- Start taking small credit and improve your credit score.

- Learn about the types of loans and why they are required.

Planned Investing

- Like other parts of finance, investing is subject to market risk. Many people refrain from investing because of its volatile nature. You must have seen many rich people say, ‘you must start investing as soon as you can’but never understood how.

- Investing is similar to buying an item for yourself. The only difference is the items you buy here increases in value, whether you buy real estate, business, stocks, bonds, or any other asset.

- However, you should understand that taking a risk and taking a calculated risk are two very separate things.

- At first, you may not understand how a company or a real estate would perform in the next 5 years, but there are many indicators and factors help you check the history and current performance of the business, analyze the market needs and based on that help you take a calculated risk on the future trend and growth of an investment.

- Losing a few hundred is no biggie if you are new to investing! But keep a note on why it happened and how you can improve it.

Risk Management

- Risk is everywhere. If you invest, you risk losing your money. If you don’t, you risk devaluating your money. So managing risk is important for financial confidence. And to take a risk, it takes courage.

- You don’t have to take the risk of losing $100,000 but start with a small amount and as you gain confidence in your financial knowledge, take a bigger risk.

Goal Setting

- Goal setting is the most important part of financial knowledge, and probably everything unitl now is futile if you don’t have a goal.

- For example, how would you know when to take out your investments? Setting a goal helps you understand your financial targets and when you reach that target, take out your money for your needs. For example, maybe you need to buy a car or house or anything with your investments.

- Setting a goal is how you achieve that goal. So set financial goals for the next 2 years, 5 years, 10 years, 20 years, or plan your retirement with it.

- Decide your goal and begin your journey. Goal setting gives direction to your financial knowledge and helps you find possibilities; otherwise, you would have skipped.

These are the 6 important elements to improve financial knowledge. Over time, you will be able to take greater risks and manage your money effectively. But, of course, falling short on cash is normal, so whenever you need an extra hand to manage your finances, get the same-day e-transfer loan in Canada from us.